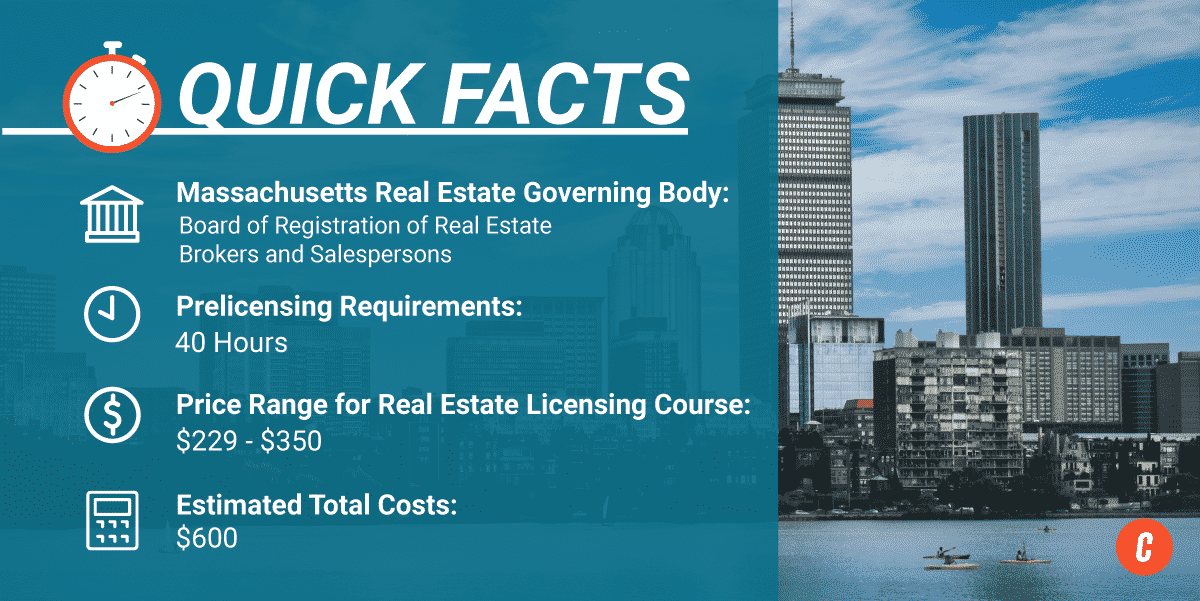

To obtain a real estate license in Oregon, you must be at least 18 years old. Additionally, you must be either a US citizen or permanent resident alien. It is also necessary to show proof of graduation from high school. To apply, you will need to pay $230. Further information can be found on the application.

Pre-licensing education

Pre-licensing education classes are required for anyone who wants to obtain an Oregon realty license. There are many choices. Some schools will give you textbooks. Others will provide video instruction. A few schools will include exam prep, but it is often more cost effective to purchase these courses separately.

OnlineEd's pre-licensure course is another option. The online course also includes MP3 audio and career resources. It also has a study schedule. PSI is the company that administers state licensing exams. The course is taught. It also offers testing facilities in Oregon.

Exam

The Oregon realty license exam is designed for you to test your knowledge and understanding of state realty laws. It is important to prepare by taking a high-quality exam prep course. A good Oregon real estate training course should be a combination of lecture videos and practice exams. These materials are divided into modular components, which include audio/visual presentations as well as reading assignments. Multiple choice questions are also included.

Six main areas are covered in the real estate law section. These areas cover ownership, land-use controls, disclosures., valuation, taxes, contracts, financing. This also includes the law that governs broker activities. It can be difficult to prepare for this exam. Fortunately, there are a number of resources and textbooks available to help you study for the exam.

Requirements

An exam and background check are required in order to obtain a Oregon real property license. The exam is broken into two sections: one for the national portion, and one for the state portion. In Oregon, you must score at least seventy percent on both portions to earn a license. The state portion of the exam contains fifty questions, and the national section has 80 questions. The pass mark for both parts is seventy-five percent.

You have two options: you can purchase individual courses and a premium package, which includes post-licensing. Each course is comprised of seven interactive modules and includes comprehensive study materials as well as practice exams. If you have previous experience in real estate, you may choose to purchase the standard package. The basic package is for those who have had previous real-estate experience. If you're new to real estate, you can buy a course that includes an introduction to business building.

Costs

Your license is required before you are allowed to work as a broker in Oregon. Your license must also be renewed every two-years. You can pay the renewal fee by credit card for $230. The background check includes fingerprinting.

Many people opt to take online pre-licensing education courses. These are self-paced with study materials. These courses offer a guarantee that you will pass your exam the first time you attempt. Prices for these courses will vary depending on the provider. It is crucial to pick the right course for your needs. It is not enough to check a box. You will want to know everything you can in order to pass the licensing exam and become a licensed agent.

Requirements in order to renew license

Before you can apply for your Oregon real-estate license renewal, you must first understand the requirements. At least 18 years old. You must submit fingerprints and go through a background check. In addition, you must have completed at least 180 hours of pre-license education. The mandatory three hour course on lead poisoning mitigation must be completed. Each two-year period, you are required to complete at least 14 hours of continuing learning.

Many resources are available online to help you prepare for the renewal of your Oregon real estate license. Kaplan Real Estate Education has online courses. You can either purchase individual courses or a complete course package. The textbooks can also be purchased. Many of these courses may be completed online, making it affordable for everyone with even modest budgets.

FAQ

What are the downsides to a fixed-rate loan?

Fixed-rate loans tend to carry higher initial costs than adjustable-rate mortgages. Additionally, if you decide not to sell your home by the end of the term you could lose a substantial amount due to the difference between your sale price and the outstanding balance.

What should I look out for in a mortgage broker

A mortgage broker is someone who helps people who are not eligible for traditional loans. They work with a variety of lenders to find the best deal. There are some brokers that charge a fee to provide this service. Others offer no cost services.

What are the benefits associated with a fixed mortgage rate?

A fixed-rate mortgage locks in your interest rate for the term of the loan. This will ensure that there are no rising interest rates. Fixed-rate loan payments have lower interest rates because they are fixed for a certain term.

Should I use an mortgage broker?

A mortgage broker may be able to help you get a lower rate. A broker works with multiple lenders to negotiate your behalf. Some brokers do take a commission from lenders. Before signing up for any broker, it is important to verify the fees.

Are flood insurance necessary?

Flood Insurance protects you from flooding damage. Flood insurance protects your belongings and helps you to pay your mortgage. Learn more information about flood insurance.

How do I calculate my interest rates?

Interest rates change daily based on market conditions. The average interest rates for the last week were 4.39%. Multiply the length of the loan by the interest rate to calculate the interest rate. For example: If you finance $200,000 over 20 year at 5% per annum, your interest rates are 0.05 x 20% 1% which equals ten base points.

Is it possible to get a second mortgage?

Yes, but it's advisable to consult a professional when deciding whether or not to obtain one. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to Find Houses to Rent

Renting houses is one of the most popular tasks for anyone who wants to move. But finding the right house can take some time. When it comes to choosing a property, there are many factors you should consider. These factors include price, location, size, number, amenities, and so forth.

You should start looking at properties early to make sure that you get the best price. For recommendations, you can also ask family members, landlords and real estate agents as well as property managers. This will ensure that you have many options.