Californians looking for a real estate license may be concerned about the price. The cost could vary from $544 to $1065. This depends on the state you are in. While some costs are fixed, others may be variable. The DRE exam fee is a fixed expense, while the real estate licensing exam fee in California can vary. However, a real estate license costs less than other professions.

California allows you to obtain a real estate license within two years. However, it must be renewed every four years. You will need to pass an exam and complete a course. An 8-hour course must be taken on fair housing practices and risk management during your first year. To keep your license valid, you must also complete 45 hours in continuing education. These courses must only be taken by an accredited institution.

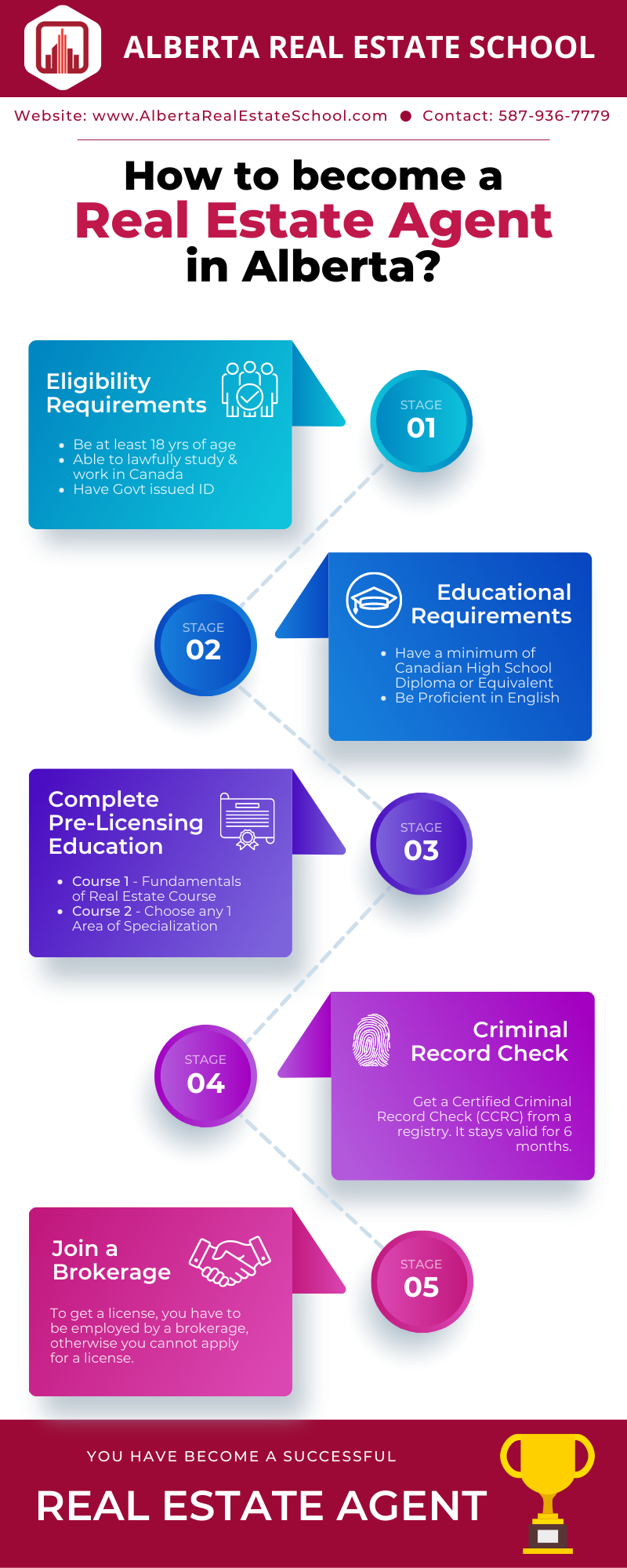

To qualify for the real estate license, you must be at least 18 years old and show a clear criminal record. You will also need to submit fingerprints and pay the appropriate fees.

The real estate license fee includes a fee for taking the DRE exam, an eight-hour crash course on real estate practices, and study materials. Some of these fees are refundable while others are not. You can pay with a credit card, check or money order.

The eLicensing platform allows applicants online to apply for their realty license. The system allows you to schedule your exam. The user can also choose the exam date, place, and time. They also have to pay the $245 licensing cost.

California's real estate market is highly competitive. You should research a broker with a track record. You might want to inquire about their retention rates and lead generation. You can also get useful guidance from a good broker.

You can improve your chances for passing the DRE exam by taking the above test prep course. Many people find it takes multiple attempts to pass. Although the real estate license cost is minimal, it isn't something to be taken lightly.

You can find a number of schools that offer pre-licensing courses. The average cost is between $125 and $700. However the price varies depending upon the provider. Online and in-person courses are available. Online courses are great for those who are short on time or need to move quickly.

It's worth the investment to get your California Real Estate License. However, before you apply, make sure that you are ready. You will need to complete a background check and fingerprinting before you can apply. Once you have the appropriate documents, you can begin the application process. Once your application has been approved, you can schedule your real estate exam.

FAQ

Should I use a broker to help me with my mortgage?

A mortgage broker can help you find a rate that is competitive if it is important to you. Brokers can negotiate deals for you with multiple lenders. Some brokers receive a commission from lenders. Before signing up for any broker, it is important to verify the fees.

What are the disadvantages of a fixed-rate mortgage?

Fixed-rate loans are more expensive than adjustable-rate mortgages because they have higher initial costs. Additionally, if you decide not to sell your home by the end of the term you could lose a substantial amount due to the difference between your sale price and the outstanding balance.

How do you calculate your interest rate?

Market conditions impact the rates of interest. In the last week, the average interest rate was 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

Can I get a second loan?

Yes. However it is best to seek the advice of a professional to determine if you should apply. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

What should I look for when choosing a mortgage broker

A mortgage broker assists people who aren’t eligible for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. This service may be charged by some brokers. Others offer no cost services.

How much should I save before I buy a home?

It depends on how much time you intend to stay there. Start saving now if your goal is to remain there for at least five more years. However, if you're planning on moving within two years, you don’t need to worry.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How do you find an apartment?

When you move to a city, finding an apartment is the first thing that you should do. This process requires research and planning. This involves researching neighborhoods, looking at reviews and calling people. Although there are many ways to do it, some are easier than others. Before renting an apartment, it is important to consider the following.

-

Researching neighborhoods involves gathering data online and offline. Online resources include websites such as Yelp, Zillow, Trulia, Realtor.com, etc. Local newspapers, landlords or friends of neighbors are some other offline sources.

-

See reviews about the place you are interested in moving to. Yelp, TripAdvisor and Amazon provide detailed reviews of houses and apartments. You can also find local newspapers and visit your local library.

-

To get more information on the area, call people who have lived in it. Ask them what they liked and didn't like about the place. Ask for their recommendations for places to live.

-

Take into account the rent prices in areas you are interested in. Renting somewhere less expensive is a good option if you expect to spend most of your money eating out. However, if you intend to spend a lot of money on entertainment then it might be worth considering living in a more costly location.

-

Learn more about the apartment community you are interested in. How big is the apartment complex? What price is it? Is it pet-friendly? What amenities does it offer? Are there parking restrictions? Are there any rules for tenants?